Best Teacher I Ever Had

by David Owen

Extracted from Reader's Digest (Asian Edition), April 1991, pp. 47-48.

Mr. Whitson taught sixth-grade science. On the first day of class, he gave us a lecture about a creature called the cattywampus, an ill-adapted nocturnal animal that was wiped out during the Ice Age. He passed around a skull as he talked. We all took notes and later had a quiz.

When he returned my paper, I was shocked. There was a big red X through each of my answers. I had failed. There had to be some mistake! I had written down exactly what Mr. Whitson said. Then I realized that everyone in the class had failed. What had happened?

Very simple, Mr. Whitson explained. He had made up all the stuff about the cattywampus. There had never been any such animal. The information in our notes was, therefore, incorrect. Did we expect credit for incorrect answers?

Needless to say, we were outraged. What kind of test was this? And what kind of teacher?

We should have figured it out, Mr. Whitson said. After all, at the every moment he was passing around the cattywampus skull (in truth, a cat's), hadn't he been telling us that no trace of the animal remained? He had described its amazing night vision, the color of its fur and any number of other facts he couldn't have known. He had given the animal a ridiculous name, and we still hadn't been suspicious. The zeroes on our papers would be recorded in his grade book, he said. And they were.

Mr. Whitson said he hoped we would learn something from this experience. Teachers and textbooks are not infallable. In fact, no one is. He told us not to let our minds go to sleep, and to speak up if we ever thought he or the textbook was wrong.

Every class was an adventure with Mr. Whitson. I can still remember some science periods almost from beginning to end. On day he told us that his Volkswagon was a living organism. It took us two full days to put together a refutation he would accept. He didn't let us off the hook until we had proved not only that we knew what an organism was but also that we had the fortitude to stand up for the truth.

We carried our brand-new skepticism into all our classes. This caused problems for the other teachers, who weren't used to being challenged. Our history teacher would be lecturing about something, and then there would be clearings of the throat and someone would say 'cattywampus.'

If I'm ever asked to propose a solution to the problems in our schools, it will be Mr. Whitson. I haven't made any great scientific discoveries, but Mr. Whitson's class gave me and my classmates something just as important: the courage to look people in the eye and tell them they are wrong. He also showed us that you can fun doing it.

Not everyone sees the value in this. I once told an elementary school teacher about Mr. Whitson. The teacher was appalled. "He shouldn't have tricked you like that," he said. I looked that teacher right in the eye and told him that he was wrong.

Friday, November 25, 2011

Ideas on Reforming the Institution of "Permanent Residency"

I recently read a lament on how the PR system has been abused ("Stop PRs from Gaming the System", The Online Citizen, 25 Nov 2011). Much anger has been generated recently by this aged and imperfect institution and I would like to offer some ideas on reforming Permanent Residency.

I take it as a fact that Singapore needs skilled workers and talented individuals from various fields. In order to make terms attractive for these individuals, they should be granted privileges similar to those Singaporeans enjoy. To me, it should not matter even if they skip out on NS. We do not need them to learn how to dig holes in the ground and fill them back up. Rather, we need them to contribute maximally. From this point of view, I would rather have freshman PAP MP Janil Puthucheary spending "the last 10 years saving kids' lives" as opposed to spending the last 7.5 years saving kids' lives and 2.5 years certifying the MCs of reasonably healthy NSFs.

The problem with the present implementation of the PR system is that there is a failure to verify. I, as a technical elitist, would argue that many PRs do not fit the description of "skilled workers" or "talented individuals". I believe that Singapore should grow in a controlled manner, taking in only those who advance our interests.

Verification cannot be entrusted to a central organization except as a rubber stamp to credible nominations. This is so clear and uncontroversial as to not require explicit supporting arguments. I believe that "enlightened self-interest" is the key to the verification of capability or talent. In particular, the "free market" will be able to judge effectively whether a potential PR can contribute sufficiently. Firms can, and will, put a dollar value on the benefit that an individual can generate. It is on this firm bedrock of rational self-interest that I propose we build our PR system.

Firms (private sector or public sector) should sponsor the Permanent Residency of their foreign staff, and those who are not deemed able to contribute should lose their PR status. Sponsorship of Permanent Residency should be expensive enough to provide a clear signal that the firm values the contribution of a PR. (For instance, it might cost, annually, some large fixed sum and plus some fixed percentage of the PR's total annual compensation.) As such, on top of a firm having to offer an attractive enough compensation (along with the promise of PR status) to attract talented foreign staff, it also has to pay a premium to certify its esteem of the capabilities of its foreign staff. This, to me, is credible verification.

Perhaps after at least 5 years of Permanent Residency, a PR might apply for citizenship contingent on continued sponsorship as a PR for a period of time (like 3 months). PRs, whose capabilities would have been credibly certified by then, would find it attractive to take it up at that point. Their employer might offer them a pay raise corresponding to a portion of what it formerly spent to certify them as skilled or talented individuals. A higher compensation package would be a material inducement. If they do not accept citizenship, they are welcome to remain PRs so long as they remain sponsored by some firm.

It is interesting how going back to fundamentals has brought us to something like the "Employment Pass" system. I believe that the intent behind that policy was to use salary as a credible signal. Unfortunately, the signals that the Ministry of Manpower decided on were less than credible as salary paybacks were used as a tool to game that system, which should also be corrected.

I would like to close by emphasizing that the privileges associated with being a PR should be attractive, but Permanent Residency should be a costly employment perk that firms offer to their foreign employees. The willingness to incur a high economic cost is a credible signal of the expectation to reap an even higher gain. Only credible signals should be used in the award of privileges like those of Permanent Residency. Economic signals like the aforementioned might be the default, but the judgment of eminent (not just qualified) figures in the relevant disciplines should be accepted as credible signals as well. All in all: credible signals, credible signals, credible signals.

I take it as a fact that Singapore needs skilled workers and talented individuals from various fields. In order to make terms attractive for these individuals, they should be granted privileges similar to those Singaporeans enjoy. To me, it should not matter even if they skip out on NS. We do not need them to learn how to dig holes in the ground and fill them back up. Rather, we need them to contribute maximally. From this point of view, I would rather have freshman PAP MP Janil Puthucheary spending "the last 10 years saving kids' lives" as opposed to spending the last 7.5 years saving kids' lives and 2.5 years certifying the MCs of reasonably healthy NSFs.

The problem with the present implementation of the PR system is that there is a failure to verify. I, as a technical elitist, would argue that many PRs do not fit the description of "skilled workers" or "talented individuals". I believe that Singapore should grow in a controlled manner, taking in only those who advance our interests.

Verification cannot be entrusted to a central organization except as a rubber stamp to credible nominations. This is so clear and uncontroversial as to not require explicit supporting arguments. I believe that "enlightened self-interest" is the key to the verification of capability or talent. In particular, the "free market" will be able to judge effectively whether a potential PR can contribute sufficiently. Firms can, and will, put a dollar value on the benefit that an individual can generate. It is on this firm bedrock of rational self-interest that I propose we build our PR system.

Firms (private sector or public sector) should sponsor the Permanent Residency of their foreign staff, and those who are not deemed able to contribute should lose their PR status. Sponsorship of Permanent Residency should be expensive enough to provide a clear signal that the firm values the contribution of a PR. (For instance, it might cost, annually, some large fixed sum and plus some fixed percentage of the PR's total annual compensation.) As such, on top of a firm having to offer an attractive enough compensation (along with the promise of PR status) to attract talented foreign staff, it also has to pay a premium to certify its esteem of the capabilities of its foreign staff. This, to me, is credible verification.

Perhaps after at least 5 years of Permanent Residency, a PR might apply for citizenship contingent on continued sponsorship as a PR for a period of time (like 3 months). PRs, whose capabilities would have been credibly certified by then, would find it attractive to take it up at that point. Their employer might offer them a pay raise corresponding to a portion of what it formerly spent to certify them as skilled or talented individuals. A higher compensation package would be a material inducement. If they do not accept citizenship, they are welcome to remain PRs so long as they remain sponsored by some firm.

It is interesting how going back to fundamentals has brought us to something like the "Employment Pass" system. I believe that the intent behind that policy was to use salary as a credible signal. Unfortunately, the signals that the Ministry of Manpower decided on were less than credible as salary paybacks were used as a tool to game that system, which should also be corrected.

I would like to close by emphasizing that the privileges associated with being a PR should be attractive, but Permanent Residency should be a costly employment perk that firms offer to their foreign employees. The willingness to incur a high economic cost is a credible signal of the expectation to reap an even higher gain. Only credible signals should be used in the award of privileges like those of Permanent Residency. Economic signals like the aforementioned might be the default, but the judgment of eminent (not just qualified) figures in the relevant disciplines should be accepted as credible signals as well. All in all: credible signals, credible signals, credible signals.

Friday, November 18, 2011

Idiocy Should be Seen Once and Never Heard of Again

In the span of less than a week, there were two furores over some things idiots said. A (now former) Young PAP member captioned a picture of some Malay kindergarteners on a bus as "young terrorist trainees" or something to that effect. Today, a police report was filed, under the Sedition Act, against someone posting an image with text featuring "strong anti-Islam sentiments".

My personal opinion (and this is really a matter of opinion) is that idiocy should be ignored and not spread. There is the perspective that strong reactions highlight what is acceptable to "us as a society". Then again there is the dynamic where unpopular views are retained but not expressed until an opportune moment with respect to the power balance. There are many ways to look at this.

To promote my view that I don't want to hear about these idiots, I'd like to say that (i) there will always be negative elements in society and life is too short to enumerate all of them, and (ii) if it was a case of "I wasn't thinking and did something stupid", I'd like us to forgive rather than embitter (in this case, I don't want additional "Muslims ruined my life" sentiments to form).

There are more important things facing our country than people saying stupid things. Long term economic viability, housing, immigration, governance, civil rights, the list goes on. I'd like to heard more debate on these from the media, mainstream or otherwise.

Wednesday, November 16, 2011

A Proposed Auction System for Public Housing

Following on from the counterfactual public housing system I previously wrote about, I would like to flesh out the auction system used to allocate HDB flats.

[Edit: But before moving on, I would like to state that I do understand that when supply can be manipulated, prices will naturally shoot up. Thus, it is important that this be executed only once there is a buffer stock of flats and only if there is explicit policy to maintain that buffer stock.]

The allocation of HDB flats will be done through the conduct of regular VCG-based auctions of all available flats in Singapore by HDB, with a reserve price on each flat set to a reasonable value reflective of cost or cost-plus. Interested buyers would first register with HDB and then be issued with accounts to bid for flats. They would then place bids for each flat they are interested in.

In what follows, I intend to recapitulate my description of the auction mechanism and how it works. Then, I will describing the kinds of outcomes generated by the auction through graphs generated from numerical experiments. Some of this will be repeated material (for which I apologize), as it is intended to make this as self-contained as possible.

Auctions and Free-Market Prices

Before moving on, I would like to emphasize that a major aim of using such an auction is to get at the true free market values of flats. I have previously mentioned that personal valuations for flats take into account both economic, relational and personal factors that are mostly unaccounted for in “independent valuations”. Furthermore, the phenomenon of substitution throws another wrench into the work of arriving at an accurate valuation. A household may be willing to consider 3-room, 4-room or 5-room flats. If valuers do not account for this, they will double (or triple) count demand, leading to artificially high values. (This insight was obtained from viewing allocation and pricing output from the auction based on various scenarios.)

While I concede that valuers may have some knowledge of substitution patterns, difficult as they might be to measure, there is little incentive to use it. Furthermore, it is a "forgivable mistake", noting the simplistic "price is determined by intersecting supply and demand" image that many have of economics.

Eliminating Dilemmas

It is, perhaps, underemphasized that potential buyers face dilemmas when flat issues are conducted in “unfortunate orders”. One’s second choice location might be up first, followed by one’s first choice. One then faces the dilemma of whether or not to apply in the first issue. The associated “what if” questions are a needless hassle. Furthermore, it stands to reason that clearing a national public housing auction is likely to increase allocative efficiency.

Characteristics of the Proposed VCG-based Auction

By allocating all available flats (old and new) through a VCG-based auction mechanism where bidders articulate their valuations for the (multiple) flat types they desire in their bids (and revise them periodically until the auction closes), the following will be achieved:

Having hopefully motivated the use of an auction mechanism to allocate flats, I would like to sketch the mechanics of the auction. Firstly, this auction mechanism will stand up easily to scrutiny because it is based on a well-known (and well-studied) family of mechanisms called Vickrey-Clarke-Groves (VCG) Mechanisms. In the auction, each bid price is intended to be the maximum amount the relevant bidder is willing to pay for a flat of a particular type in a particular location. Bidders will make bids for every type of flat they are interested in.

The outcome of the auction will be the socially optimal allocation based on the bids made and subject to allocation constraints that HDB has such as reserved quantities for first timers and the Ethnic Integration Policy (EIP). This leads to the achievement of (i).

Furthermore, it may be said that only preferences of buyers and the constraints of the (non-profit seeking) HDB are incorporated into the allocation. As such, the input of external parties seeking to profit off the outcome of the auction is minimized, in all it is arguable that this leads to (ii).

The pricing of each allocated flat is done via externality pricing. That is to say, for each winning bidder, the maximum social welfare of all bidders is computed again with the winning bidder removed. Necessarily, this new number is never larger than the maximum social welfare when all bidders are included. Call the difference between these numbers w. The price that bidder pays is his bid less w. With some thought, it would be clear that had he bid anything more that the price he paid, allocating him that flat would certainly remain part of the optimal allocation, and had he bid less, allocating him that flat would no longer be part of the optimal allocation. For mechanism design neophytes, it may require a bit more time to understand this argument, but it explains (iii). From a different perspective, it stands to reason that the optimal bidding strategy is for a bidder to truthfully bid the actual maximum value he is willing to pay for a flat, and the auction mechanism will not use this information to extract additional revenue from him.

This leads to a major criticism of the VCG Mechanism by academics and auction practitioners: revenue from VCG-based auctions compares poorly to that from other auction forms. This arises as VCG enforces the property of truthfulness by charging winning bidders the lowest amount they could have bid and been allocated a flat, an amount typically much lower than the amount bid, as mentioned in the explanation of (iii). However, having less revenue extracted from winning bidders turns out to be a strength for allocating public housing. Since the mission of HDB is to "provide affordable homes of quality and value", it may be said that selling flats at the reserve price is a mark of successfully meeting housing demand in an affordable fashion and low revenue from the auction is not, in fact, a problem.

Consider conducting the auction in manner where the tentative outcome for one’s bids and the tentative prices for flats in each category are made available at regular intervals, and bidders are able to update their bids in response to tentative outcomes. It cannot be assumed that people have full clarity on the real value of a flat to them. By viewing a tentative outcome, they may realize that they are willing to pay more for a flat of a particular type, or that they have overvalued a flat of a particular type. This explains (iv). It is suggested that prior to the close of the auction, there be a (long) period where results are no longer updated to reduce the incentive of last minute “sniping”.

The Allocation Model for our VCG-based Auction

The Allocation Model is basically defines the characteristics of the socially optimal allocation, expressing it as a mixed-integer linear optimization problem, the objective of which is to pick an allocation which maximizes the total sum of the bids corresponding to allocated flats. Note, however, that the price of the flat is at most the bid price and usually strictly lower.

The parameters that define the problem are:

vij: Bid price of bidder i for a flat of category j

mj: Number of available flats in category j

ojr: Maximum of available flats in category j that members of racial group r may buy

... and the variables that define the allocation:

xij: Boolean variable defining whether bidder i was allocated a flat in category j (for the bidder representing HDB, this is a not a boolean variable, but rather a non-negative integer variable)

So, the following optimization problem is to be solved using linear optimization software: (I know I said that this is an integer program, but the linear relaxation is equivalent. This can be easily shown by an appeal to the Ghouila-Houri characterization of Total Unimodularity, which proves that optimizing any linear objective over the above feasible set can be done efficiently.)

maximize Sum[over bidders i and flat categories j] vij xij

subject to:

The set of constraints (1) mean that each bidder (other than HDB) may be allocated at most 1 flat. The set of constraints (2) mean that all flats are allocated. The set of constraints (3) serves to reserve some fraction of flats for first timers. This in turn results in higher prices on second timers due to the higher externality they will impose on other second timers when allocated flats. The set of constraints (4) reflects the government's “Ethnic Integration Policy” (EIP). The inclusion of (4) will probably translate the previous time to sell/time to buy difference for different ethnic groups to a price difference. With this constraint, it would really pay to be among more of those of other races.

One can prove that if the bid prices (other than HDB's) are all not equal (and other non-equal "difference" conditions hold), this integer optimization problem can be relaxed to an equivalent linear optimization problem. (This can be easily engineered and implies big computational savings, which will be necessary for quickly producing an allocation and pricing the allocated flats.) Such a scenario can be engineered by requiring minimal bid increments (of say $100) and incorporating random tie breaking by doctoring bids by random values smaller than the bid increment. This practical measure is similar to allocating flats by ballot, but differs in that it first takes allocative efficiency into account.

Examples

Having outlined the characteristics of the auction, allow me to provide some concrete (albeit simple) examples of bids and outcomes. If only 800 bidders compete for an issue of 1000 "identical" flats, regardless of how wildly high some bidders might bid, all bidders bidding at least the reserve price pay just the reserve price for their flat. In contrast, if 1800 bidders compete for an issue of 1000 "identical" flats, all bidding more than the reserve price, the 1000 winning bidders would end up paying the 1001-st highest bid price. In the setting of auctioning identical items, the VCG auction reduces to the k-th price auction.

One might visualize the results by using bid prices to describe "demand" and relating it to the quantity of the respective type of flat supplied. Notably, this auction tends to see winning bidders paying less than the price determined by the point where the (assumed vertical) supply curve intersects the "demand curve". This is due to substitution effects, as HDB flats of different types are related goods. This is true for all bidders when no first timer and EIP constraints are included, when those constraints are included this would still typically be true for the first timers.

Now let us look at some auction results. The graphs that follow will depict demand for a type of flat (bid prices), fulfillment (allocation of flats at some price), flat supply for this type of flat, and the reserve price for this type of flat. I've neglected to label the axes, but the vertical axis denotes price and the horizontal axis denotes quantity.

The first example (Figure 1) is a fairly pedestrian one. This particular instance reflects supply exceeding demand for this type of flat, so all demand is satisfied at the reserve price.

Figure 5: Flat Category C1 from a Small Example with EIP Constraints and Unbalanced Demand from Ethnic Groups

Figure 5: Flat Category C1 from a Small Example with EIP Constraints and Unbalanced Demand from Ethnic Groups

Hopefully the above examples have been helpful in illustrating how the auction behaves. While some of the examples suggest that prices can get high, I would like to assure the reader that they only get high in the event that supply is inadequate. The fact is, examples with adequate supply are boring, probably with all flats selling at or near the reserve price, these were constructed to exhibit "interesting behavior".

[Edit: But before moving on, I would like to state that I do understand that when supply can be manipulated, prices will naturally shoot up. Thus, it is important that this be executed only once there is a buffer stock of flats and only if there is explicit policy to maintain that buffer stock.]

The allocation of HDB flats will be done through the conduct of regular VCG-based auctions of all available flats in Singapore by HDB, with a reserve price on each flat set to a reasonable value reflective of cost or cost-plus. Interested buyers would first register with HDB and then be issued with accounts to bid for flats. They would then place bids for each flat they are interested in.

In what follows, I intend to recapitulate my description of the auction mechanism and how it works. Then, I will describing the kinds of outcomes generated by the auction through graphs generated from numerical experiments. Some of this will be repeated material (for which I apologize), as it is intended to make this as self-contained as possible.

Auctions and Free-Market Prices

Before moving on, I would like to emphasize that a major aim of using such an auction is to get at the true free market values of flats. I have previously mentioned that personal valuations for flats take into account both economic, relational and personal factors that are mostly unaccounted for in “independent valuations”. Furthermore, the phenomenon of substitution throws another wrench into the work of arriving at an accurate valuation. A household may be willing to consider 3-room, 4-room or 5-room flats. If valuers do not account for this, they will double (or triple) count demand, leading to artificially high values. (This insight was obtained from viewing allocation and pricing output from the auction based on various scenarios.)

While I concede that valuers may have some knowledge of substitution patterns, difficult as they might be to measure, there is little incentive to use it. Furthermore, it is a "forgivable mistake", noting the simplistic "price is determined by intersecting supply and demand" image that many have of economics.

Eliminating Dilemmas

It is, perhaps, underemphasized that potential buyers face dilemmas when flat issues are conducted in “unfortunate orders”. One’s second choice location might be up first, followed by one’s first choice. One then faces the dilemma of whether or not to apply in the first issue. The associated “what if” questions are a needless hassle. Furthermore, it stands to reason that clearing a national public housing auction is likely to increase allocative efficiency.

Characteristics of the Proposed VCG-based Auction

By allocating all available flats (old and new) through a VCG-based auction mechanism where bidders articulate their valuations for the (multiple) flat types they desire in their bids (and revise them periodically until the auction closes), the following will be achieved:

- (i) information about multiple flat types is integrated in the pricing and allocation outcome, (ii) a truly free-market allocation is arrived at, (iii) allocated flats are priced at the lowest possible bid which could have been made without changing the outcome, and (iv) each bidder gains a better picture of his/her preferences as the auction progresses.

Having hopefully motivated the use of an auction mechanism to allocate flats, I would like to sketch the mechanics of the auction. Firstly, this auction mechanism will stand up easily to scrutiny because it is based on a well-known (and well-studied) family of mechanisms called Vickrey-Clarke-Groves (VCG) Mechanisms. In the auction, each bid price is intended to be the maximum amount the relevant bidder is willing to pay for a flat of a particular type in a particular location. Bidders will make bids for every type of flat they are interested in.

The outcome of the auction will be the socially optimal allocation based on the bids made and subject to allocation constraints that HDB has such as reserved quantities for first timers and the Ethnic Integration Policy (EIP). This leads to the achievement of (i).

Furthermore, it may be said that only preferences of buyers and the constraints of the (non-profit seeking) HDB are incorporated into the allocation. As such, the input of external parties seeking to profit off the outcome of the auction is minimized, in all it is arguable that this leads to (ii).

The pricing of each allocated flat is done via externality pricing. That is to say, for each winning bidder, the maximum social welfare of all bidders is computed again with the winning bidder removed. Necessarily, this new number is never larger than the maximum social welfare when all bidders are included. Call the difference between these numbers w. The price that bidder pays is his bid less w. With some thought, it would be clear that had he bid anything more that the price he paid, allocating him that flat would certainly remain part of the optimal allocation, and had he bid less, allocating him that flat would no longer be part of the optimal allocation. For mechanism design neophytes, it may require a bit more time to understand this argument, but it explains (iii). From a different perspective, it stands to reason that the optimal bidding strategy is for a bidder to truthfully bid the actual maximum value he is willing to pay for a flat, and the auction mechanism will not use this information to extract additional revenue from him.

This leads to a major criticism of the VCG Mechanism by academics and auction practitioners: revenue from VCG-based auctions compares poorly to that from other auction forms. This arises as VCG enforces the property of truthfulness by charging winning bidders the lowest amount they could have bid and been allocated a flat, an amount typically much lower than the amount bid, as mentioned in the explanation of (iii). However, having less revenue extracted from winning bidders turns out to be a strength for allocating public housing. Since the mission of HDB is to "provide affordable homes of quality and value", it may be said that selling flats at the reserve price is a mark of successfully meeting housing demand in an affordable fashion and low revenue from the auction is not, in fact, a problem.

Consider conducting the auction in manner where the tentative outcome for one’s bids and the tentative prices for flats in each category are made available at regular intervals, and bidders are able to update their bids in response to tentative outcomes. It cannot be assumed that people have full clarity on the real value of a flat to them. By viewing a tentative outcome, they may realize that they are willing to pay more for a flat of a particular type, or that they have overvalued a flat of a particular type. This explains (iv). It is suggested that prior to the close of the auction, there be a (long) period where results are no longer updated to reduce the incentive of last minute “sniping”.

The Allocation Model for our VCG-based Auction

The Allocation Model is basically defines the characteristics of the socially optimal allocation, expressing it as a mixed-integer linear optimization problem, the objective of which is to pick an allocation which maximizes the total sum of the bids corresponding to allocated flats. Note, however, that the price of the flat is at most the bid price and usually strictly lower.

The parameters that define the problem are:

vij: Bid price of bidder i for a flat of category j

mj: Number of available flats in category j

ojr: Maximum of available flats in category j that members of racial group r may buy

... and the variables that define the allocation:

xij: Boolean variable defining whether bidder i was allocated a flat in category j (for the bidder representing HDB, this is a not a boolean variable, but rather a non-negative integer variable)

So, the following optimization problem is to be solved using linear optimization software: (I know I said that this is an integer program, but the linear relaxation is equivalent. This can be easily shown by an appeal to the Ghouila-Houri characterization of Total Unimodularity, which proves that optimizing any linear objective over the above feasible set can be done efficiently.)

maximize Sum[over bidders i and flat categories j] vij xij

subject to:

- Sum[over flat categories j] xij ≤ 1 for each bidder i except HDB (1)

- Sum[over bidders i] xij = mj for each flat category j (2)

- Sum[over bidders i in racial group r] xij ≤ ojr for each flat category j and racial group r (4)

The set of constraints (1) mean that each bidder (other than HDB) may be allocated at most 1 flat. The set of constraints (2) mean that all flats are allocated. The set of constraints (3) serves to reserve some fraction of flats for first timers. This in turn results in higher prices on second timers due to the higher externality they will impose on other second timers when allocated flats. The set of constraints (4) reflects the government's “Ethnic Integration Policy” (EIP). The inclusion of (4) will probably translate the previous time to sell/time to buy difference for different ethnic groups to a price difference. With this constraint, it would really pay to be among more of those of other races.

One can prove that if the bid prices (other than HDB's) are all not equal (and other non-equal "difference" conditions hold), this integer optimization problem can be relaxed to an equivalent linear optimization problem. (This can be easily engineered and implies big computational savings, which will be necessary for quickly producing an allocation and pricing the allocated flats.) Such a scenario can be engineered by requiring minimal bid increments (of say $100) and incorporating random tie breaking by doctoring bids by random values smaller than the bid increment. This practical measure is similar to allocating flats by ballot, but differs in that it first takes allocative efficiency into account.

Examples

Having outlined the characteristics of the auction, allow me to provide some concrete (albeit simple) examples of bids and outcomes. If only 800 bidders compete for an issue of 1000 "identical" flats, regardless of how wildly high some bidders might bid, all bidders bidding at least the reserve price pay just the reserve price for their flat. In contrast, if 1800 bidders compete for an issue of 1000 "identical" flats, all bidding more than the reserve price, the 1000 winning bidders would end up paying the 1001-st highest bid price. In the setting of auctioning identical items, the VCG auction reduces to the k-th price auction.

One might visualize the results by using bid prices to describe "demand" and relating it to the quantity of the respective type of flat supplied. Notably, this auction tends to see winning bidders paying less than the price determined by the point where the (assumed vertical) supply curve intersects the "demand curve". This is due to substitution effects, as HDB flats of different types are related goods. This is true for all bidders when no first timer and EIP constraints are included, when those constraints are included this would still typically be true for the first timers.

Now let us look at some auction results. The graphs that follow will depict demand for a type of flat (bid prices), fulfillment (allocation of flats at some price), flat supply for this type of flat, and the reserve price for this type of flat. I've neglected to label the axes, but the vertical axis denotes price and the horizontal axis denotes quantity.

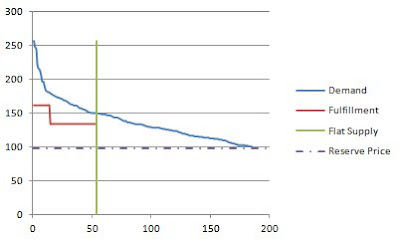

The first example (Figure 1) is a fairly pedestrian one. This particular instance reflects supply exceeding demand for this type of flat, so all demand is satisfied at the reserve price.

Figure 1: Supply exceeds demand

Figure 1: Supply exceeds demand

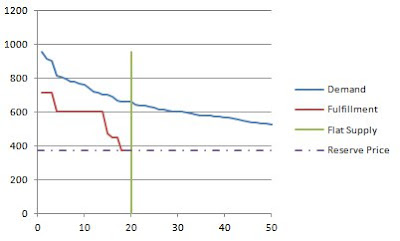

The next examples (Figure 2 and Figure 3) are part of a small-medium sized example with 2000 bidders (1712 of whom made at least 1 bid) competing for 521 flats in 10 categories. (Data was randomly generated.) About 40% of the bidders are second timers and for each flat category, at most 15% to 30% of the flats may be allocated to second timers. The EIP constraints were not imposed.

In Figure 2, one sees that 13 bidders paid 146 for their flats while the other 44 paid 115. The former group were all second timers, while the latter were all first timers. This illustrates the effect of restricting the number of flats available to a certain group. A similar effect is visible in Figure 3, from the same example. In general, with k "groups" with different constraints on each, one would expect to see k price levels in the fulfillment curve.

Figure 2: Flat Category C0 from a Small-Medium Sized Example

Figure 3: Flat Category C4 from a Small-Medium Sized Example

Figure 3: Flat Category C4 from a Small-Medium Sized Example

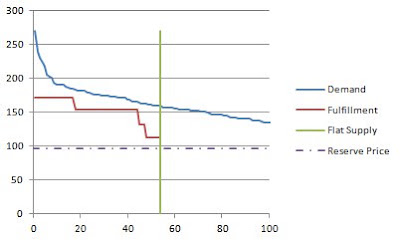

The next examples (Figure 4 and Figure 5) are part of a small-medium sized example with 2000 bidders (1476 of whom made at least 1 bid) competing for 297 flats in 10 categories. (Again, data was randomly generated.) About 40% of the bidders are second timers and for each flat category, at most 15% to 30% of the flats may be allocated to second timers. Each flat category was restricted to 70% Chinese buyers, 15% Malay buyers and 10% Indian buyers. However, 80% of the bidders were Chinese, 5% were Malay and 10% were Indian.

In Figures 4 and 5, one sees multiple price levels, corresponding to different subsets of bidders, with each group facing different forms of restriction that increase, in varying degrees, the level of competition for flats between bidders in the respective subsets. In both figures, the highest prices are paid by the second timer ethnic Chinese buyers, due to the restrictions placed on them and the higher competition for available flats within their ethnic group.

Figure 4: Flat Category C0 from a Small Example with EIP Constraints and Unbalanced Demand from Ethnic Groups

Figure 5: Flat Category C1 from a Small Example with EIP Constraints and Unbalanced Demand from Ethnic Groups

Figure 5: Flat Category C1 from a Small Example with EIP Constraints and Unbalanced Demand from Ethnic GroupsHopefully the above examples have been helpful in illustrating how the auction behaves. While some of the examples suggest that prices can get high, I would like to assure the reader that they only get high in the event that supply is inadequate. The fact is, examples with adequate supply are boring, probably with all flats selling at or near the reserve price, these were constructed to exhibit "interesting behavior".

The small-medium example of Figures 2-3 took about 5 sec to solve per optimization problem using an open source solver (GLPK). With about 500 allocations, it actually took just under 50 min to compute the pricing decisions for each flat allocated. A more realistic example with about 15000 bidders competing for about 5000 flats takes about 5 min to solve. However, to generate tentative prices in the auction prices for each and every flat allocated need not be computed. With parallization, much larger instances could be solved to allow tentative results to be refreshed every hour. Commercial software (CPLEX/Gurobi/Xpress MP) might be used if they're found to be much faster.

Closing Remarks

In my assessment, this auction mechanism is technically feasible and produces sensible results. I think this is worthy of exploration as a means for allocating flats in our public housing system.

In presenting this and advocating for it I do bear in mind a certain cautionary note, as so well put by Malcolm Gladwell, against the "infatuation with the things we make". We all have our blinders. With that in mind, I would like to receive comments on this especially those that point out what I've missed.

Tuesday, November 15, 2011

Late Payment, Adverse Incentives and Monetary Policy

A letter was written to the Straits Times Forum on Sat 12 Nov 2011 titled "Pay first, repaid last policy is unfair". The subject matter is rather obvious. I wrote back to the Forum with comments, my letter appeared in today's (15th Nov) issue of the papers (a day when it seemed that no one in my office touched the newspapers before 4pm). Let me give the gist of what I was trying to say:

I wrote that it may be time for Singapore to deal with the underlying problem. I said that the MAS should determine whether deferred payments may be considered reserve capital. (Yes, money could be used for other things, but I thought pointing to reserve capital as something tangible would make sense.) If the response turns out to be "no", incentives for such, arguably dishonest, corporate behaviour would be reduced.

One thing that one might learn in an introductory finance class is the value of holding other people's money. In particular, that one should watch one's cash flow, as some large clients are apt to make late payments. For insurers and other financial institutions, holding other people's money for longer times serves to artificially boost one's capital ratio. Hence, there exist incentives for insurers and other financial institutions to make late payment. (The same applies to B2B transactions, but these are harder to regulate and have less direct impact on "the citizen".)

This is a real concern. Laws do exist to limit the time banks can hold deposits before making them available to write cheques on. The Expedited Funds Availability Act in the USA is an example of this that addresses a particular face of this form of moral hazard. I previously heard an anecdote of some bank(s) in the USA being found guilty, a number of decades ago, of wrongdoing by their sending payment (in the form of cheques via snail mail) from the furthest branch away from the destination in order to have access to the customer's money for a day or so more. The sheer volume of payments made this profitable. Insurance and other financial transactions are similar. Long processing times seem like a weak excuse.

This is a real concern. Laws do exist to limit the time banks can hold deposits before making them available to write cheques on. The Expedited Funds Availability Act in the USA is an example of this that addresses a particular face of this form of moral hazard. I previously heard an anecdote of some bank(s) in the USA being found guilty, a number of decades ago, of wrongdoing by their sending payment (in the form of cheques via snail mail) from the furthest branch away from the destination in order to have access to the customer's money for a day or so more. The sheer volume of payments made this profitable. Insurance and other financial transactions are similar. Long processing times seem like a weak excuse.

I wrote that it may be time for Singapore to deal with the underlying problem. I said that the MAS should determine whether deferred payments may be considered reserve capital. (Yes, money could be used for other things, but I thought pointing to reserve capital as something tangible would make sense.) If the response turns out to be "no", incentives for such, arguably dishonest, corporate behaviour would be reduced.

Monday, November 14, 2011

Public Transport and Queueing Systems

Queueing systems are systems where demand arrives with inter-arrival times (distributed according to some probability distribution; perhaps independent, perhaps correlated, perhaps time dependent). On arrival, demand is served by one or more servers with service completing after some duration (also distributed according to some probability distribution).

There are as many kinds of queueing systems as one might imagine, but they do have one characteristic in common. Before stating it explicitly, let me introduce the M/M/1 queue, where interarrival times and service times are both distributed according to the exponential distribution, but with different parameters.

The M/M/1 queue is the first queue that engineers learn about, and the arrival rate (a) and the service rate (s) fully determine the behaviour of the queue. Now, the mean number of customers in the system at any given time is finite (i.e.: the queue length doesn't grow unboundedly with time) if and only if a < s, which is intuitive as you can't have a finite average queue length if arrivals come in faster than you can serve them. The mean waiting time is, in fact 1 / (s - a), which informs us that as demand rises and approaches service capacity, the mean waiting time in the queue grows very very fast. The analogy is clear.

It is clear that the public transport system is some form of queueing system with complicated behaviour. If we increase the vehicle population such that demand approaches capacity, we court disaster. The simple relation 1 / (s - a), does not hint at congestion being linear in demand, in fact the derivative of that expression with respect to demand gives us 1 / (s - a)2, which tells us that congestion growth accelerates at a frightening rate as we get close to capacity.

Emergency rooms in the USA formerly tried to match demand with capacity, but met with huge problems when demand surged. Now, they cater some additional capacity to deal with these surges.

I'm unsure why we continue overloading our road network, but the disaster that will befall us when demand reaches capacity will not come slowly and gradually. It will be like stepping off a cliff: sudden and spectacular. (Gridlock is, afterall, quite a sight.)

----

Afternote: I actually wrote this in response to a TOC article on the MRT network. Interestingly, the MRT network is not quite near capacity yet (in the queueing sense), so only a rather big increase in peak hour capacity will alleviate the crowding situation. The road network is what we need to watch out for. We need real engineers in charge of such systems. This is important.

Thursday, November 10, 2011

A Counterfactual Public Housing System (Revised)

(This is a revised version of a previous post containing a revised auction mechanism with nice properties, including strategy-proof-ness. An edited version of this was published at NewAsiaRepublic.)

I would like to examine a counterfactual. What if, in Singapore, public housing were more tightly controlled by HDB in the following fashion:

A Counterfactual Public Housing System

The resale price (back to HDB) for a flat would be set according to its type and floor area. Thus, a 1000 square feet four-room flat in Marine Parade would be sold back to HDB for the same amount as a 1000 square feet four-room flat in Pasir Ris. Furthermore, these resale prices would be kept low. (This may be tweaked to account for age and recent upgrading work.) The purchase of flats would be done by sealed-bid auction, with the previously mentioned resale price as the reserve price. (The details of the auction mechanism will be outlined in the Annex.) In addition, if an owner of a HDB flat comes to own any private property in Singapore (through purchase or bequest), that person must dispose of either the HDB flat (to HDB) or the private property.

Due to the low resale prices, there would be no incentive to purchase HDB flats for speculative purposes. Presently, there is a loophole where some foreign nationals (PRs and those with dual citizenships) are essentially able to buy to rent, reducing the strained public housing supply and profiting off the misery of the "flat-less". Measures to plug that loophole will be outlined in the next paragraph. On the other hand, to avoid market distortions where a flat is priced at the same amount as a less desirable one, sale of flats will be done by (country-wide) auction (with a reserve price dictated by the nature of the flat). It is intended that buyers make bids for available flats of all types in all locations so as to eliminate dillemas of whether to participate in an auction for flats of a second choice type or in a second choice location. All this would serve to "defragment" the public housing market and ensure that the premium paid over the reserve price reflects desirability due to location, and does not contain a component pricing potential future speculative profit.

To reduce actual foreign speculative pressure, consider requiring all flat owners holding any foreign citizenships (non-citizens and citizens with dual citizenships) to certify their occupancy of their flats by certifying, in person, every quarter (or some suitable time interval), their occupancy of their flat at their local town council. This will not be onerous as town councils are typically located close by.

The philosophy behind this counterfactual system is that residents derive value from public housing based on the housing space and the location. The actual public housing market, comprising the buyers, is best equipped to price this premium. Hence the auction mechanism. The premium paid over the resale price would reflect the value derived from the flat consumed by the owner over the tenure of residence and, as such, would not be returned when the flat is sold back to HDB.

Implications for Economic Vibrancy and Investment

It follows that without a concomitant increase in prices and without an accompanying fall in wages, lower housing prices will result in higher household savings. (The former two do not appear to follow from lower housing prices.)

The upshot of this is that funds would be available for the enterprising to start businesses. The less entrepreneurial would have funds to invest in those new businesses. With less funds tied up in property, the economic landscape would be fertile enough to encourage new businesses to spring forth and be nourished by the increased availability of funds.

It is not too much of a stretch to project that a number of these new businesses would introduce innovative business models and new uses of technology, thus bringing a new vibrancy to the economy. With this, investment in Singapore will no far less property driven, but rather, innovation led, as befits a knowledge economy.

Closing Remarks

The counterfactual public housing system I have proposed has a number of positive features. However, the problem is how to get from the present state to this one. In my mind, the way forward entails a number of steps (i) legislate that the divestment requirement for all public housing to take effect in a number of years (as existing current legislation to that effect is not retroactive), (ii) begin a two-speed public housing market where the resale of all new flats will be based on this paradigm and current flats can be sold to other buyers or to HDB at the aforementioned resale price.

Step (ii) will result in a gradual conversion of the public housing market to the aforementioned counterfactual system. In decades to come, as newer, more desirable, flats are rolled out, the prices of current flats will naturally decline due to the greater availability of cheaper flats, as well as their age. Eventually they will be sold back to HDB at the dictated resale price, reducing the share of flats held in the old housing system.

Will this take place? It depends on the priorities of the government and the electorate.

At first glance, it might appear that the use of auctions would punish poorer Singaporeans based on the historical use of auctions for selling collectors' items. However, auctions are a direct mechanism to mark to market. Auctions have been used for certain types of items that are difficult to properly value a priori, such as collectors' items whose market value is uncertain. Homes are similar to an extent. HDB and banks cannot properly assess how much value a flat has to a buyer as work location, residents of friends and family, and a host of other factors contribute to this.

I envision the conduct of regular auctions of all available flats in Singapore with the reserve price on each flat set to the aforementioned resale price. Interested buyers would first register with HDB and then be issued with accounts to bid for flats. They would then place bids for each flat they are interested in.

This is my third attempt. The first attempt at a mechanism is featured at the previous post. It was not satisfactory. The second was online just briefly, but was taken down because I realized that an aspect of the proof of strategy-proof-ness was wrong and it couldn't be fixed. (I found a clear counterexample.) This auction mechanism will stand up easily to scrutiny because it is based on a well-known (and well-studied) family of mechanisms called Vickrey-Clarke-Groves (VCG) Mechanisms.

In the auction, each bid price is intended to be the maximum amount the relevant bidder is willing to pay for a flat of a particular type in a particular location. Bidders will make bids for every type of flat they are interested in. The beauty of VCG mechanisms is that the optimal bidding strategy is for a bidder to truthfully bid the actual maximum value he is willing to pay for a flat, the auction mechanism will not use this information to extract additional revenue from him. This is in contrast to situations where perfect price discrimination is possible and buyers have an incentive to hide information on exactly how much they are willing to pay.

To jump the gun, the allocation portion of the auction seeks to maximize allocative efficiency, which is quantified by the total value of the allocation to the bidders defined by the sum of bid prices for all allocated flats (including unallocated flats which are valued at the reserve price. The pricing portion charges each bidder allocated a flat a price which represents "the social cost to society of him having been allocated the flat". Imprecisely speaking, this social cost typically entails the loss to someone else who would have been allocated a flat, and as such, is typically the bid price of the bidder "next in line" to be allocated a flat (the first among the losing bidders). More accurately, the price charged for each allocated flat is precisely the lowest amount the respective bidder could have bid and been allocated the flat.

Annex: The Allocation Model for the VCG Auction

nj: Number of available flats in category j

maximize Sum[over i and j] vij xij

subject to:

The set of constraints (1) mean that each bidder (other than HDB) may be allocated at most 1 flat. The set of constraints (2) mean that all flats are allocated.

One can prove that if the bid prices (other than HDB's) are all not equal (and another non-equal "difference" condition holds), this integer optimization problem can be relaxed to a linear optimization problem and yield the same solution. (This can be easily engineered and implies big computational savings, which will be necessary for quickly producing an allocation and pricing the allocated flats.) Such a scenario can be engineered by requiring minimal bid increments (of say $100) and incorporating random tie breaking by doctoring bids by random values smaller than the bid increment. This practical measure is similar to allocating flats by ballot, but differs in that it first takes allocative efficiency into account.

I would like to examine a counterfactual. What if, in Singapore, public housing were more tightly controlled by HDB in the following fashion:

- purchase and sale transactions could only be performed with HDB itself,

- prices were controlled so as to preserve only market forces based on location-based desirability to individual buyers while, at the same time, removing the speculative component.

A Counterfactual Public Housing System

The resale price (back to HDB) for a flat would be set according to its type and floor area. Thus, a 1000 square feet four-room flat in Marine Parade would be sold back to HDB for the same amount as a 1000 square feet four-room flat in Pasir Ris. Furthermore, these resale prices would be kept low. (This may be tweaked to account for age and recent upgrading work.) The purchase of flats would be done by sealed-bid auction, with the previously mentioned resale price as the reserve price. (The details of the auction mechanism will be outlined in the Annex.) In addition, if an owner of a HDB flat comes to own any private property in Singapore (through purchase or bequest), that person must dispose of either the HDB flat (to HDB) or the private property.

Due to the low resale prices, there would be no incentive to purchase HDB flats for speculative purposes. Presently, there is a loophole where some foreign nationals (PRs and those with dual citizenships) are essentially able to buy to rent, reducing the strained public housing supply and profiting off the misery of the "flat-less". Measures to plug that loophole will be outlined in the next paragraph. On the other hand, to avoid market distortions where a flat is priced at the same amount as a less desirable one, sale of flats will be done by (country-wide) auction (with a reserve price dictated by the nature of the flat). It is intended that buyers make bids for available flats of all types in all locations so as to eliminate dillemas of whether to participate in an auction for flats of a second choice type or in a second choice location. All this would serve to "defragment" the public housing market and ensure that the premium paid over the reserve price reflects desirability due to location, and does not contain a component pricing potential future speculative profit.

To reduce actual foreign speculative pressure, consider requiring all flat owners holding any foreign citizenships (non-citizens and citizens with dual citizenships) to certify their occupancy of their flats by certifying, in person, every quarter (or some suitable time interval), their occupancy of their flat at their local town council. This will not be onerous as town councils are typically located close by.

The philosophy behind this counterfactual system is that residents derive value from public housing based on the housing space and the location. The actual public housing market, comprising the buyers, is best equipped to price this premium. Hence the auction mechanism. The premium paid over the resale price would reflect the value derived from the flat consumed by the owner over the tenure of residence and, as such, would not be returned when the flat is sold back to HDB.

Implications for Economic Vibrancy and Investment

It follows that without a concomitant increase in prices and without an accompanying fall in wages, lower housing prices will result in higher household savings. (The former two do not appear to follow from lower housing prices.)

The upshot of this is that funds would be available for the enterprising to start businesses. The less entrepreneurial would have funds to invest in those new businesses. With less funds tied up in property, the economic landscape would be fertile enough to encourage new businesses to spring forth and be nourished by the increased availability of funds.

It is not too much of a stretch to project that a number of these new businesses would introduce innovative business models and new uses of technology, thus bringing a new vibrancy to the economy. With this, investment in Singapore will no far less property driven, but rather, innovation led, as befits a knowledge economy.

Closing Remarks

The counterfactual public housing system I have proposed has a number of positive features. However, the problem is how to get from the present state to this one. In my mind, the way forward entails a number of steps (i) legislate that the divestment requirement for all public housing to take effect in a number of years (as existing current legislation to that effect is not retroactive), (ii) begin a two-speed public housing market where the resale of all new flats will be based on this paradigm and current flats can be sold to other buyers or to HDB at the aforementioned resale price.

Step (ii) will result in a gradual conversion of the public housing market to the aforementioned counterfactual system. In decades to come, as newer, more desirable, flats are rolled out, the prices of current flats will naturally decline due to the greater availability of cheaper flats, as well as their age. Eventually they will be sold back to HDB at the dictated resale price, reducing the share of flats held in the old housing system.

Will this take place? It depends on the priorities of the government and the electorate.

Annex: Remarks on the Merits of Using Auctions for Allocating Public Housing

At first glance, it might appear that the use of auctions would punish poorer Singaporeans based on the historical use of auctions for selling collectors' items. However, auctions are a direct mechanism to mark to market. Auctions have been used for certain types of items that are difficult to properly value a priori, such as collectors' items whose market value is uncertain. Homes are similar to an extent. HDB and banks cannot properly assess how much value a flat has to a buyer as work location, residents of friends and family, and a host of other factors contribute to this.

It might be argued that current market prices cannot be said to be true free market prices. They are essentially monopoly prices set by the "housing establishment" which includes developers and banks who both profit from "high valuations". Current prices also include premiums for potential future gains.

In contrast, if buyers know they cannot resell flats to HDB for much more than the set resale price (as only small corrections are made due to inflation), then the premium they would indicate that they are willing to pay over the reserve prices would really comprise just the benefit derived from the availability of the flat to them for their planned time horizon.

Furthermore, a bidder pays at most the bid price, and in subsets of an issue which are not oversubscribed, essentially everyone (bidding for flats in those subsets) pays the reserve price. Only when there are wildly oversubscribed segments can prices get high, and only for flats in those segments.

The reserve price is intended to be a statement by HDB of cost or cost+, and that HDB will not sell for anything less than that. It should reflect the economies of scale associated with good contracting practice and good management of outsourcing contracts (i.e. costs should be low).

Annex: Remarks on Managing the Cost of Public Housing

Procurement and the management of outsourcing contracts must improve to ensure that costs to HDB, and hence flat buyers, do not increase in an unwarranted fashion. Public officials in such roles should have their incentives explicitly linked to ensuring that costs do not go up (or go down due to productivity improvements). This is aimed at eliminating the mentality that as long as the lowest cost alternative in the tender gets the award, the job is done. Such a mentality demonstrates the "not my own money" view of using public money and should be eliminated using proper incentives.

Public officials in such roles should be rewarded for keeping costs in place, and given large bonuses when costs go down (as they have generated huge value for the public). These officials should be replaced when cost increases are not supportable by market conditions. Furthermore, exclusion clauses should exist to prevent them, for a period of time, from working for construction firms, firms in closely related industries, companies linked by a parent company or in a parent-child relationship with such firms. All this serves to prevent collusion that harms the public.

Annex: An Attempt at an Auction Mechanism

I envision the conduct of regular auctions of all available flats in Singapore with the reserve price on each flat set to the aforementioned resale price. Interested buyers would first register with HDB and then be issued with accounts to bid for flats. They would then place bids for each flat they are interested in.

This is my third attempt. The first attempt at a mechanism is featured at the previous post. It was not satisfactory. The second was online just briefly, but was taken down because I realized that an aspect of the proof of strategy-proof-ness was wrong and it couldn't be fixed. (I found a clear counterexample.) This auction mechanism will stand up easily to scrutiny because it is based on a well-known (and well-studied) family of mechanisms called Vickrey-Clarke-Groves (VCG) Mechanisms.

In the auction, each bid price is intended to be the maximum amount the relevant bidder is willing to pay for a flat of a particular type in a particular location. Bidders will make bids for every type of flat they are interested in. The beauty of VCG mechanisms is that the optimal bidding strategy is for a bidder to truthfully bid the actual maximum value he is willing to pay for a flat, the auction mechanism will not use this information to extract additional revenue from him. This is in contrast to situations where perfect price discrimination is possible and buyers have an incentive to hide information on exactly how much they are willing to pay.

To jump the gun, the allocation portion of the auction seeks to maximize allocative efficiency, which is quantified by the total value of the allocation to the bidders defined by the sum of bid prices for all allocated flats (including unallocated flats which are valued at the reserve price. The pricing portion charges each bidder allocated a flat a price which represents "the social cost to society of him having been allocated the flat". Imprecisely speaking, this social cost typically entails the loss to someone else who would have been allocated a flat, and as such, is typically the bid price of the bidder "next in line" to be allocated a flat (the first among the losing bidders). More accurately, the price charged for each allocated flat is precisely the lowest amount the respective bidder could have bid and been allocated the flat.

To give a concrete (albeit simple) example, if only 800 bidders compete for an issue of 1000 "identical" flats, regardless of how wildly high some bidders might bid, all bidders bidding at least the reserve price pay the reserve price for their flat. In contrast, if 1800 bidders compete for an issue of 1000 "identical" flats, the 1000 winning bidders would end up paying the 1001-st highest bid price. In the setting of auctioning identical items, the VCG auction reduces to the k-th price auction. One might visualize the results to be exactly "intersecting the demand curve with the supply curve" to determine the equilibrium price. This justifies the claim that such a mechanism is a direct (and accurate) means to price flats through the free market.

One criticism of the VCG Mechanism turns out to be a strength for allocating public housing: revenue from VCG-based auctions compares poorly to that from other auction forms. This arises as VCG enforces the property of truthfulness by charging winning bidders the lowest amount they could have bid and been allocated a flat, an amount typically much lower than the amount bid. Since the mission of HDB is to "provide affordable homes of quality and value", it may be said that selling flats at the reserve price is a mark of successfully meeting housing demand in an affordable fashion and low revenue from the auction is not, in fact, a problem.

If this takes off, there will probably be a short lived cottage industry of housing agents offering bidding services for flats, but with proper communication of what the optimal bidding strategy is, this market inefficiency (due to lack of awareness) will disappear.

In the future, I will probably post examples of the VCG auction at work.

Annex: The Allocation Model for the VCG Auction

vij: Bid price of bidder i for a flat of category j

xij: Boolean variable defining whether bidder i was allocated a flat in category j (for the bidder representing HDB, this is a not a boolean variable, but rather a non-negative integer variable)nj: Number of available flats in category j

maximize Sum[over i and j] vij xij

subject to:

- Sum[over flat categories j] xij <= 1 for each bidder i except HDB (1)

Sum[over bidders i] xij = nj for each flat category j (2)

The set of constraints (1) mean that each bidder (other than HDB) may be allocated at most 1 flat. The set of constraints (2) mean that all flats are allocated.

One can prove that if the bid prices (other than HDB's) are all not equal (and another non-equal "difference" condition holds), this integer optimization problem can be relaxed to a linear optimization problem and yield the same solution. (This can be easily engineered and implies big computational savings, which will be necessary for quickly producing an allocation and pricing the allocated flats.) Such a scenario can be engineered by requiring minimal bid increments (of say $100) and incorporating random tie breaking by doctoring bids by random values smaller than the bid increment. This practical measure is similar to allocating flats by ballot, but differs in that it first takes allocative efficiency into account.

Saturday, November 5, 2011

Where the Public Housing System Should Be (With Diagrams!)

I'd like to make a quick comment on where I think the public housing system to be. The following diagram depicts the public housing market without specification of the number of flats supplied. (The market here consists of all Singaporean households with household incomes lower than the income ceiling.)

With a low flat supply, only those who are willing to pay are able to get flats. Prices are high and much of the viable demand is not served due to scarcity effects. (... where viable demand denotes the number of flats that could be sold given market demand.) The above diagram reflects the perfect price discrimination scenario, which leaves no consumer surplus. (Somehow the shape of the postulated demand curve leaves little room for any consumer surplus even in the event of all falts transacting at the "equilibrium supply-mets-demand price.)

The reserve price would be the price below which HDB would not be willing to sell, reflecting cost or cost-plus. Now, I would like to consider the simple situation where all sale transactions involve purchases from HDB. With that, let me compare "low supply" with "high supply". Suppose that allocation is done according to the "most reliable market signal" of willingness to pay. Now let us consider "low supply".

Of course, all flats are sold. Now consider "high supply".

Now, many more people can get a flat. Note that the surplus flat buffer allows for all flats to be sold at the reserve price. All viable demand is satisfied. One can see that some people without the means to pay still cannot get flats. Additional government measures may help more people to get flats, up to the flat supply. This has already been done through the creation of another housing market with a lower income ceiling. As for the rest who still fall through the cracks, I don't know. My sense is that a Singapore version of the New Deal could work.

Now, many more people can get a flat. Note that the surplus flat buffer allows for all flats to be sold at the reserve price. All viable demand is satisfied. One can see that some people without the means to pay still cannot get flats. Additional government measures may help more people to get flats, up to the flat supply. This has already been done through the creation of another housing market with a lower income ceiling. As for the rest who still fall through the cracks, I don't know. My sense is that a Singapore version of the New Deal could work.

I think the last diagram illustrates where I would like the public housing system to be. It better illustrates fulfilment of the first line of the HDB mission statement ("We provide affordable homes of quality and value"). In so far as this is a main objective of public housing, this is where we should be. HDB is doing well by ramping up supply.

Tuesday, November 1, 2011

A Counterfactual Public Housing System and Its Outcomes

Today, I would like to examine a counterfactual. What if, in Singapore, public housing were more tightly controlled by HDB. In particular, what if purchase and sale transactions could only be performed with HDB itself and prices were controlled so as to preserve market forces based on location-based desirability while, at the same time, relieving speculative pressure. Let me elaborate on the basic mechanism behind this.

A Counterfactual Public Housing System

The sale price for a flat would be fixed upfront, according to its type and floor area. Thus, a 1000 square feet four-room flat in Marine Parade would be sold back to HDB for the same amount as a 1000 square feet four-room flat in Pasir Ris. Furthermore, these sale prices would be kept low. (This may be tweaked to account for age and recent upgrading work.) The purchase of flats would be done by sealed-bid auction, with the previously mentioned sale price as the reserve price. (The details of the auction mechanism will be outlined in the Annex.) In addition, if an owner of a HDB flat comes to own any private property in Singapore (through purchase or bequest), that person must dispose of either the HDB flat (to HDB) or the private property.

Due to the low, fixed sale prices, there would be no incentive to purchase HDB flats for speculative purposes. Presently, there is a loophole where some foreign nationals (PRs and those with dual citizenships) are essentially able to buy to rent, reducing the strained public housing supply and profiting off the misery of the "flat-less". Measures to plug that loophole will be outlined in the next paragraph. On the other hand, to avoid market distortions where a flat is priced at the same amount as a less desirable one, sale of flats will be done by (country-wide) auction (with a reserve price dictated by the nature of the flat). All this serve to ensure that the premium paid over the reserve price reflects desirability due to location, and does not contain a component pricing potential future speculative profit.

To reduce actual foreign speculative pressure, consider requiring all flat owners holding any foreign citizenships (non-citizens and citizens with dual citizenships) to certify their occupancy of their flats by certifying, in person, every quarter (or some suitable time interval), their occupancy of their flat at their local town council. This will not be onerous as town councils are typically located close by.

The philosophy behind this counterfactual system is that residents derive value from public housing based on the housing space and the location. The actual housing market, comprising the buyers, is best equipped to price this premium. Hence the auction mechanism. The premium paid over the sale price would reflect the value derived from the flat consumed by the owner over the tenure of residence and, as such, would not be returned when the flat is sold back to HDB.

Implications for Economic Vibrancy and Investment

It follows that without a concomitant increase in prices and without an accompanying fall in wages, lower housing prices will result in higher household savings. (The former two do not appear to follow from lower housing prices.)

The upshot of this is that funds would be available for the enterprising to start businesses. The less entrepreneurial would have funds to invest in those new businesses. With less funds tied up in property, the economic landscape would be fertile enough to encourage new businesses to spring forth and be nourished by the increased availability of funds.

A Counterfactual Public Housing System

The sale price for a flat would be fixed upfront, according to its type and floor area. Thus, a 1000 square feet four-room flat in Marine Parade would be sold back to HDB for the same amount as a 1000 square feet four-room flat in Pasir Ris. Furthermore, these sale prices would be kept low. (This may be tweaked to account for age and recent upgrading work.) The purchase of flats would be done by sealed-bid auction, with the previously mentioned sale price as the reserve price. (The details of the auction mechanism will be outlined in the Annex.) In addition, if an owner of a HDB flat comes to own any private property in Singapore (through purchase or bequest), that person must dispose of either the HDB flat (to HDB) or the private property.

Due to the low, fixed sale prices, there would be no incentive to purchase HDB flats for speculative purposes. Presently, there is a loophole where some foreign nationals (PRs and those with dual citizenships) are essentially able to buy to rent, reducing the strained public housing supply and profiting off the misery of the "flat-less". Measures to plug that loophole will be outlined in the next paragraph. On the other hand, to avoid market distortions where a flat is priced at the same amount as a less desirable one, sale of flats will be done by (country-wide) auction (with a reserve price dictated by the nature of the flat). All this serve to ensure that the premium paid over the reserve price reflects desirability due to location, and does not contain a component pricing potential future speculative profit.

To reduce actual foreign speculative pressure, consider requiring all flat owners holding any foreign citizenships (non-citizens and citizens with dual citizenships) to certify their occupancy of their flats by certifying, in person, every quarter (or some suitable time interval), their occupancy of their flat at their local town council. This will not be onerous as town councils are typically located close by.